This is a project I did with my friend and colleague — Wiam FOUAZ. In this research, we looked into Microsoft's second-largest acquisition since 2016. By using two methods: Comparable analysis and DCF, we were able to estimate Nuance's EV before the deal.

Deal Overview

On April 12, Microsoft Corp (NasdaqGS: MSFT) announced its plan to acquire Nuance Communication Inc (NasdaqGS: NUAN) at $19.79 billion (including Nuance’s net debt), setting its record for the second-largest acquisition after Linkedin in 2016. The transaction will be done 100% by cash. Although the purchase price at $56 per share did not meet Nuance’s initial target, it represents a 23% premium to the firm’s closing price on April 9. The deal is expected to close by the end of this year.

The acquisition will double Microsoft’s total addressable market (TAM) in the healthcare provider space, bringing the company’s TAM in healthcare to nearly $500 billion. Nuance and Microsoft will deepen their existing commitments to the extended partner ecosystem, as well as the highest standards of data privacy, security and compliance.

Upon closing, Microsoft expects Nuance’s financials to be reported as part of Microsoft’s Intelligent Cloud segment. Microsoft expects the acquisition to be minimally dilutive (less than 1 percent) in fiscal year 2022 and to be accretive in fiscal year 2023.

Goldman Sachs & Co. LLC is acting as exclusive financial advisor to Microsoft, while Simpson Thacher & Bartlett LLP is acting as its legal advisor. Evercore is acting as exclusive financial advisor to Nuance, while Paul, Weiss, Rifkind, Wharton & Garrison LLP is acting as its legal advisor.

Source: Microsoft.com

Industry Overview

The global Healthcare IT market size was valued at USD 74.2 billion in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 10.7% over the forecast period. High demand and adoption of preventive care along with increasing funding for various mobile health startups is advancing the market growth. In addition, growing network coverage and rising improvements in network infrastructure are supporting the growth of this market. Technological advancements, with respect to healthcare, for improving the IT infrastructure, such as the implementation of AI, IoT, and big data in healthcare processes, are also fueling the market growth.

The global Artificial Intelligence market size was valued at USD 39.9 billion in 2019 and is expected to grow at a compound annual growth rate (CAGR) of 42.2% from 2020 to 2027. The continuous research and innovation directed by the tech giants are driving the adoption of advanced technologies in industry verticals, such as automotive, healthcare, retail, finance, and manufacturing. However, technology has always been an essential element for these industries, but AI has brought technology to the center of organizations.

Tech giants like Amazon.com, Inc.; Google LLC; Apple Inc.; Facebook; International Business Machines Corporation; and Microsoft are investing significantly in the research and development of AI. These companies are working for making AI more accessible for enterprise use-cases.

Source: Grand View Research

Company Analysis

Microsoft develops, manufactures, licenses, supports, and sells computer software, personal computers, and related services.

Microsoft was founded by Bill Gates and Paul Allen on April 4, 1975. It rose to dominate the personal computer operating system market with MS-DOS in the mid-1980s, followed by Microsoft Windows.

The company’s 1986 initial public offering (IPO), and subsequent rise in its share price, created three billionaires and an estimated 12,000 millionaires among Microsoft employees. Since the 1990s, it has made a number of corporate acquisitions, their largest being the acquisition of LinkedIn for $26.2 billion in December 2016, followed by their acquisition of Skype Technologies for $8.5 billion in May 2011.

Key Financials:

- Revenues (2020): $153.28bn (+14.2% compared to 2019)

- EBIT (2020): $60.16bn (EBIT margin: 39.2%)

- Net income (2020): $51.31bn (+33.5% compared to 2019)

- Net Debt (2020): -$49.2bn

- EV/EBITDA: 26.0x

- Market capitalization: $1,969.65bn (Apr. 26, 2021)

- Share price: $261.15 (Apr. 26, 2021)

Source: S&P Capital IQ

Nuance is a trusted cloud and AI software leader representing decades of accumulated healthcare and enterprise AI experience.

The company that would become Nuance was incorporated in 1992 as Visioneer. In 1999, Visioneer acquired ScanSoft, Inc., and the combined company became known as ScanSoft. In September 2005, ScanSoft Inc. acquired and merged with Nuance Communications, a natural language spinoff from SRI International.

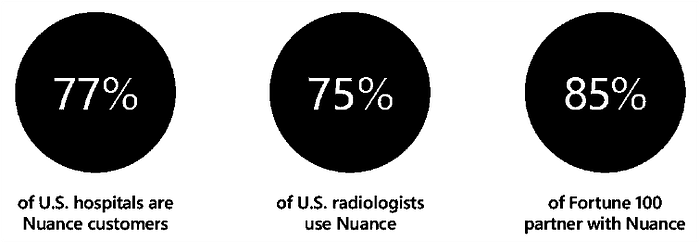

Nuance is a pioneer and a leading provider of conversational AI and cloud-based ambient clinical intelligence for healthcare providers. The Company works With various organizations across healthcare, financial services, telecommunications, government, and retail. The company operates through three segments: Healthcare, Enterprise, and Other.

Their solutions are currently used by :

Key Financials:

- Revenues (2020): $1.48bn (-16.68% compared to 2019)

- EBIT (2020): $112.62m (EBIT margin: 7.6%)

- Net income (2020): $21.71m (-90.0% compared to 2019)

- Net Debt (2020): $1.31bn

- EV/EBITDA: 68.7x

- Market capitalization: $15.16bn (Apr. 26, 2021)

- Share price: $53.09 (Apr. 26, 2021)

Valuation Method

To value the target firm in this deal, we used 2 different methods: The comparable analysis using multiples and the Discounted Cashflow (DCF).

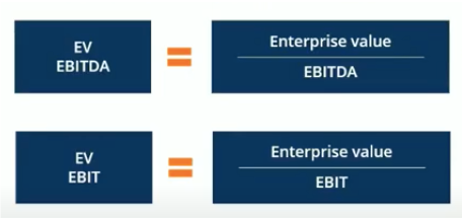

Comparable company analysis (also called “trading multiples” or “peer group analysis”) is a relative valuation method comparing the current value of a business to other similar businesses by looking at trading multiples like P/E, EV/EBITDA, or other ratios. Multiples of EBITDA are the most common valuation method. The “comps” valuation method provides an observable value for the business, based on what companies are currently worth. Comps are the most widely used approach, as they are easy to calculate and always current.

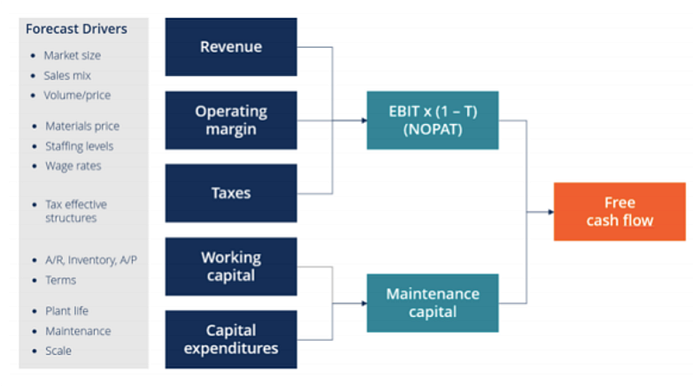

DCF method requires more studies and which takes into consideration a significant number of financial parameters; This is a so-called “intrinsic” valuation method because it is essentially based on elements relating to the company under study. The idea is to calculate the target firm’s Unlevered Free Cash Flow (FCFF) based on forecast drivers of business valuation then discount back to its present value to determine the enterprise value.

Source: Corporate Finance Institute

1. Comparable Analysis

Comp Screening

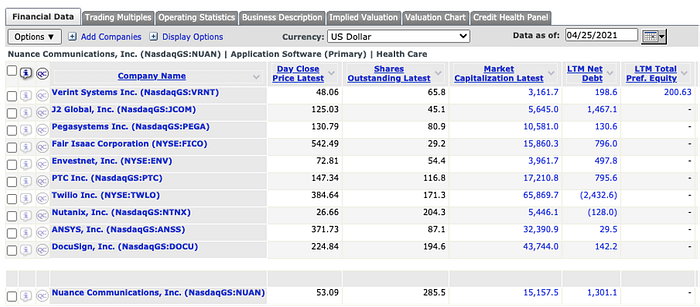

Using a combination of Quick Comps and Screening function in CapitalIQ, we set up Nuance’s Comp Set based on 4 main criteria: Industry, Segment, Geographic Locations, and Market Capitalization. This gave the result of 5 companies within the Healthcare Industry Software/Application Software, which are headquartered in the US and have market capitalization ranging from $ 10,000 million — $ 22,000 million. The selected companies share similarities in terms of Market Capitalization, Revenue, EBITDA & EBIT.

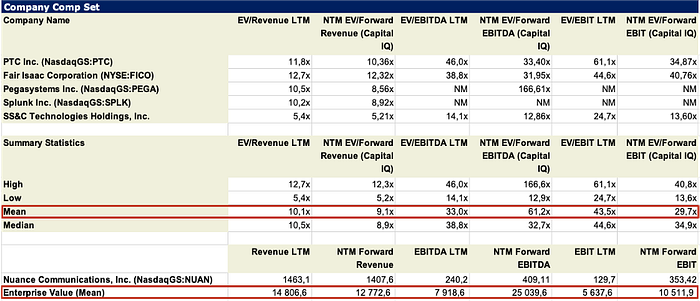

Comparable trading Multiples & Implied Valuation

In this part, we used EV/Revenue, EV/EBITDA & EV/EBIT multiples to calculate the mean value of the comp set. The implied valuation of Nuance Communications can then be determined by multiplying the mean value of each multiple vs its corresponding statistics.

The multiples and figures are the firms’ actual last twelve-month data and forecast for the next twelve-month period.

Source: S&P Capital IQ

2. Discounted Cashflow (DCF)

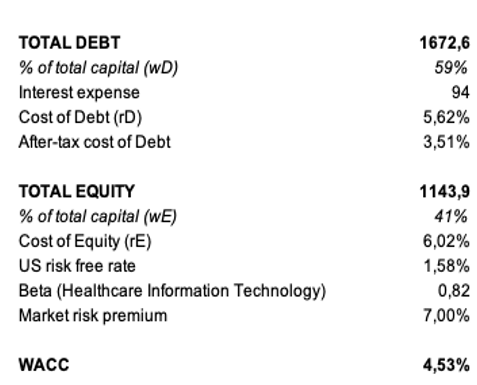

Nuance’s capital structure is made of 59% Debt and 41% Equity.

The reported total debt in 2020 was $1672,6 million (S&P CapitalIQ). The firm paid a total of $94 million in interest expense, resulting in the cost of Debt 5,62% (before tax).

The company’s cost of Equity (expected return) was calculated using the CAPM model, based on US 10 year treasury yield (treasury.gov) and US market risk (statista.com). From then the company’s WACC can be computed with the formula:

with:

wD: % of Debt

wE: % of Equity

rD: Cost of Debt

rE: Cost of Equity

(Source: CapitalIQ, statista.com, treasury.gov)

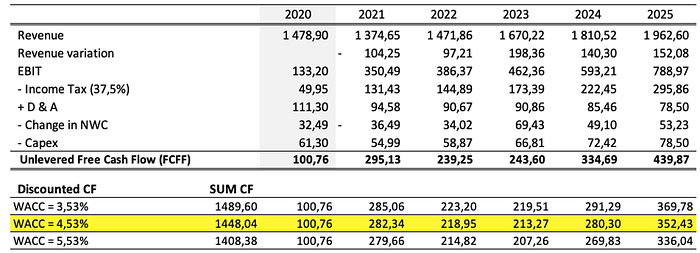

In order to compute the firm’s discounted future cash flows, we estimated the firm’s revenue & EBIT in a 5-year period, from 2021–2025, based on actual data of 2020, taking into consideration the nature of the industry. We also made different assumptions on the WACC to see how cash flows and EV vary in correlation with the change in WACC.

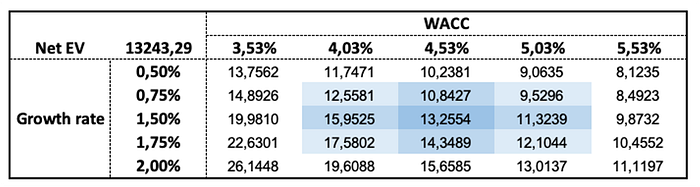

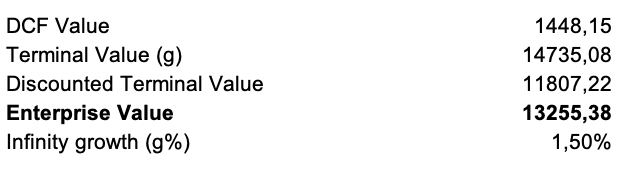

The firm value was calculated as the sum of all discounted cash flows and the terminal value taken into account the infinity growth assumption of 1.5% ($ 13.2 billion).

Sensitivity Table

Finally, we proceeded a sensitivity test to see the change in EV with 2 variables: The WACC and the perpetual growth rate, with the WACC ranging from 3.53% — 5.53% and the perpetual growth rate ranging from 0.50% — 2.00%.